ING Sustainable Finance Pulse - issue 10

30 June 2026

Reading time: 6 min

Welcome to ING’s Sustainable Finance Pulse - a quarterly glimpse into the world of sustainable finance and ING’s take on it.

In this issue:

- 1.0 Slower start sustainable finance market

- 2.0 Solid Q1 for ING

- 3.0 Hydrogen: The missing link between ambition and investment

- 4.0 ING Research: What could reduce gas reliance?

The sustainable finance market started on a slower note in the first quarter of 2026. Looking at the rest of the year, ING Research believes the issuance will remain resilient and sees a positive quarter in sustainable finance activities.

This Sustainable Finance Pulse also highlights the topic of hydrogen and how ING helps clients turn the potential of hydrogen and other clean molecules into practical progress by combining financing, advice and sector insight.

1.0 Slower start to the year for sustainable finance issuance

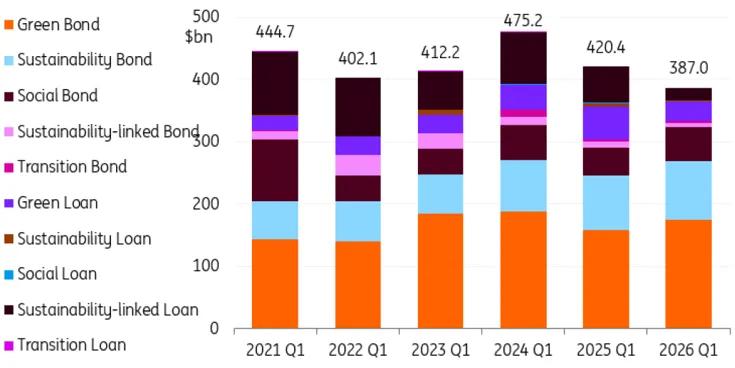

Global sustainable finance issuance started 2026 on a softer note but remained resilient, with Q1 issuance totalling US$387bn. This is around 8% lower than Q1 2025 and below all levels seen since 2021. The weakness is not uniform across issuer types.

- Non-financial corporates remained the largest issuer group, with US$103bn of issuance, but this was down sharply from US$153bn in Q1 2025.

- Financial issuance also declined to US$72bn, while supranational issuance fell to US$47bn, compared with US$82bn last year.

- The clear bright spot was government-related issuance, which almost doubled YoY to US$99bn, up from US$51bn in Q1 2025 and the strongest quarter of the past six years. This made government-related entities the second-largest source of sustainable finance issuance.

- Sovereign issuance also improved, reaching US$55bn, compared with US$40bn last year. Public-sector and quasi-public issuers provided an important anchor to the market at the start of the year.

- From an instrument perspective, the bond market held up relatively well.

- Green bonds remained the dominant instrument, with issuance reaching US$175bn, up around 11% year-on-year and representing around 45% of total sustainable finance issuance.

- Sustainability bonds also increased to US$94bn, while social bonds rose to US$54bn.

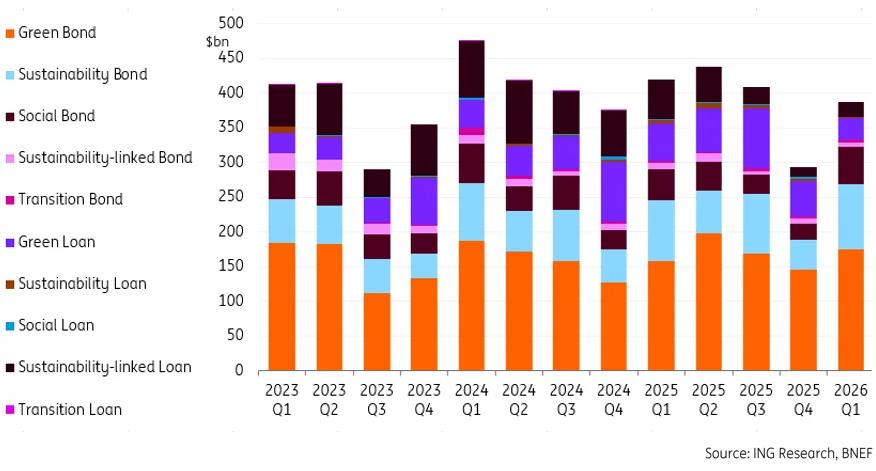

In contrast, private market activity was notably weaker. Green loan issuance fell to US$30bn, down from US$54bn in Q1 2025, while sustainability-linked loans declined sharply to US$20bn, compared with US$58bn last year. However, we do note that there may be some under-reporting within the private market side, and these figures may not reflect the full issuance levels. As a result, loans accounted for only around 14% of total sustainable finance issuance in Q1 2026, versus almost 28% in Q1 2025. We do note however that private loan transactions may not be fully captured in the dataset. In terms of region, we still see the change in trends with the US seeing a slight slowdown, but EMEA is ticking upwards.

Overall, Q1 2026 points to a softer but resilient start for the global sustainable finance market, but not a uniformly weak one. Corporate and loan-market activity declined, while government-related and sovereign issuance provided resilience.

Looking forward, we expect issuance will remain relatively strong for 2026. In particular now, as the conflict in the Middle East is showing signs of positivity, which will ultimately reduce volatility and uncertainty. The varied regional, product and issuer trends are likely to remain.

Global sustainable finance issuance by product (excluding ABS)

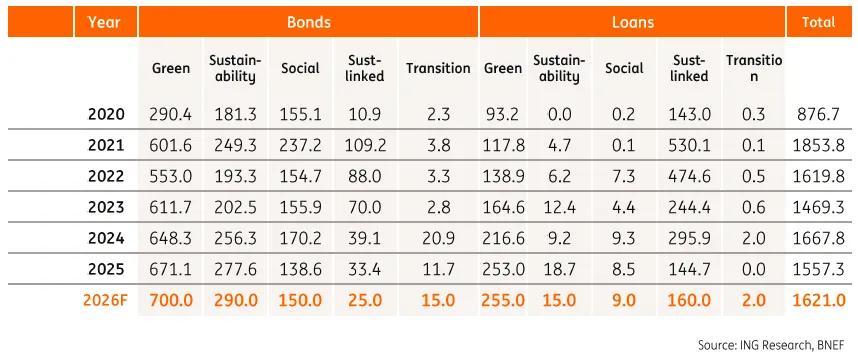

Global sustainable finance issuance in numbers (excluding ABS)

ING Global Head of Sustainable Solutions Group

Peter Kindt

"It is encouraging to see clients continuing to invest in their transition plans, even in a more uncertain market environment. Companies are taking practical steps to finance renewables, scale new technologies and build more resilient value chains. We are proud to support them on that journey."

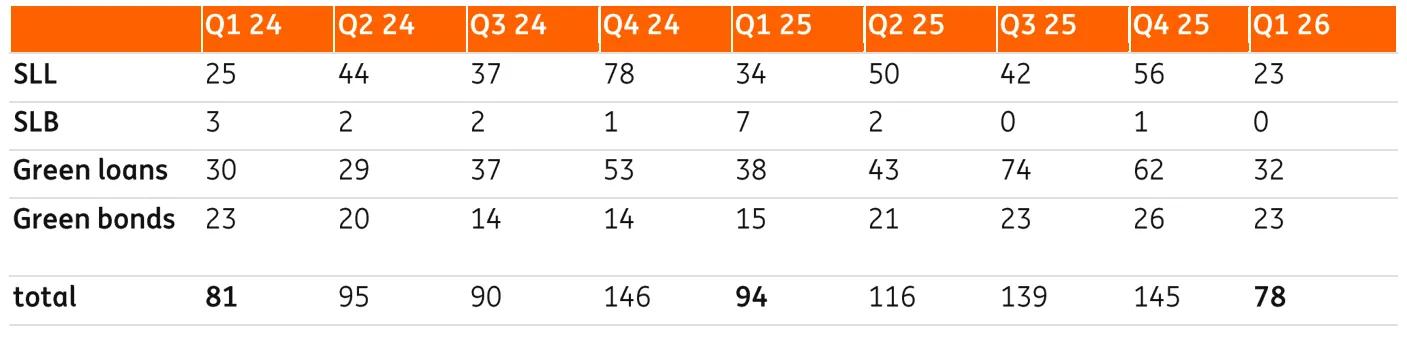

ING Sustainable Finance transactions

*Nr. of sustainable finance transactions of 4 most common sustainabilityproducts chosen by our clients

2.0 Growth and resilience underpins positive Q1

ING delivered a solid quarter, mobilising €33.7bn* in the first quarter of 2026, an 11% year-on-year increase compared to Q1 2025. Across the four products shown, we saw a slight slowdown in transaction numbers to 78, down from 94 in Q1 2025, but still ahead of the Q1 2022–2025 average of 74.

Sustainability-linked loans remain the largest contributor to volume mobilised, followed by green loans and then green bonds, together accounting for 80% of volume mobilised. Growth continues to be driven by green loans and bonds, with an uptick also seen in sustainable commercial paper and guarantee products. While the sustainability-linked loan market appears under pressure, it remains a core client engagement tool for ING, with activity proving resilient and broadly comparable to historical first quarter performance.

The disappearance of sustainability-linked bond activity is temporary, as we see them return in Q2, and we continue to view them as an appropriate product for a number of issuers, albeit with volumes expected to remain limited.

The EMEA region led with 55% of mobilised volume, followed by the Americas (33%) and APAC (8%).

In Q1, EMEA and APAC showed resilient but slightly lower volumes compared to the previous year, with the Americas driving much of the Q1 growth despite the market and political backdrop. This growth came from fewer but larger green financings in the renewables space. EMEA remains our largest and most mature market, where we continue to see a shift to quality. APAC expects volumes to continue to tick upwards, reflecting positive traction across all sustainable finance products. The market has started to discuss resilience and adaptation significantly more and, following the closure of the Strait of Hormuz, we are seeing a significant pick-up in electric vehicles(EV) sales across the APAC region.

Despite geopolitical uncertainty and shifting climate policy, many organisations continue to view sustainability as a strategic priority. We remain dedicated to helping finance these investments, scale new technologies and the value chains around them, and mobilise the capital needed to turn innovation into viable, global solutions.

*For more information and a full list of products please see: Opens in a new tabPerformance and reporting | ING

3.0 Hydrogen: The missing link between ambition and investment

Hydrogen remains a niche market but the challenge facing it is huge: not technology, but robust policy support to spur long-term demand. While clean hydrogen is seen as a key enabler of the energy transition, especially in hard-to-abate sectors such as steel,chemicalsand shipping, investment is still struggling to keep pace with ambition.

Bankability

The reason is simple: projects are not yet sufficiently bankable, something which will be required to scale this market. The technology exists, but marketsremainimmature, with limited pricing transparency, trading hubsand, above all, notenough reliable demand. For lenders and investors, that means one thing: uncertain revenues.

Demand gap

That demand gap is now the sector’s biggest obstacle. Many projects lack long-term offtake agreements with creditworthy buyers, making it hard to secure financing and move towards final investmentdecision. Policy support can help, but unless it improvesrevenuecertainty, progress is likely to remain slow.

How to unlock investment

Our article Hydrogen: How to bridge the gap between ambition and investment? argues that hydrogen’s path to scale can learn from past transitions in the energy markets, resembling the early development of LNG, but also what we consider today as ‘traditional’ renewables, wind and solar. Namely: gradual, contract-ledand dependent on the steady build-out of real markets.

To unlock investment, the focus now needs to shift from ambition to execution, by anchoring demand, stabilisingrevenues, allocating risk more realistically and building regional ecosystems where supply and demand can grow together.

Our role

In the end, ING wants to help its clients by bridging the gap between potential and progress. By combining financing, adviceand sector insight, we aim to support clients as hydrogen and other clean molecules move from early promise towards practical implementation in the real economy.

Hydrogen no longer needs to prove the technology works. It needs bankable projects, credible demand and the right risk-sharing. That is what will turn potential into scale.

- shares Henry Rushton, Sustainable Solutions Group - Energy Lead at ING.

ING supported:

- The renewable gas company Opens in a new tabVireo with a transaction that supportsthe production of bio-LNG from local waste streams for heavy transport and marine use

- Opens in a new tabSkyNRG with the world’s first greenfield sustainable aviation fuel plant to secure project financing

- Opens in a new tabTESSAF that converts TotalEnergies’ Grandpuits refinery near Paris into a zero-crude biorefinery capable of producing SAF at scale

Across these deals, ING played a financing role in projects that advance lower-carbon fuels, strengthen European clean energy supply chains and help make emerging transition technologies commercially bankable.

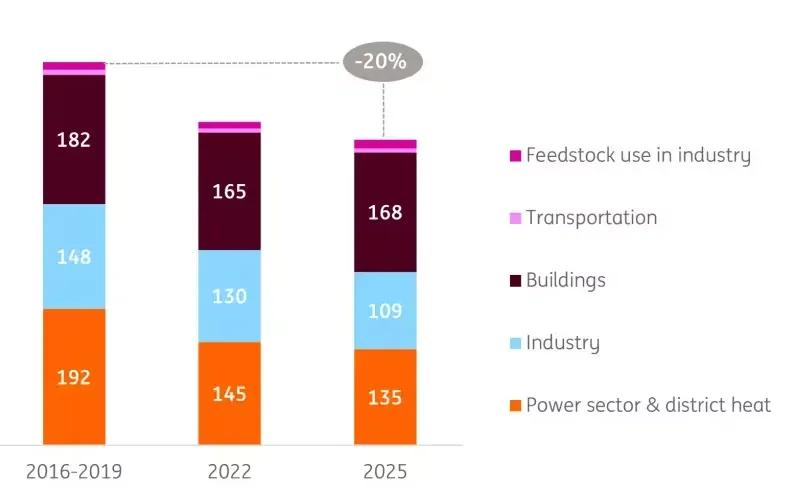

4.0 ING Research: Renewables and biogas could reduce gas reliance

Gerben Hieminga, ING’s sector economist on energy transition, takes a closer look at how Europe can reduce its reliance on expensive gas imports. He finds that the answer lies in both green electrons and green molecules such as biogas.

Until recently, much of the energy transition has taken place in the power sector. Countries such as Spain, the Netherlands and the UK now generate around half of their electricity from wind and solar. After the 2022 energy crisis, renewables accelerated sharply, and the current focus on energy security is likely to reinforce that trend. Batteries are enabling the next phase of wind and solar growth by balancing daily fluctuations in output and easing grid congestion. Coal-fired power plants may see a short-lived uptick in use, but overall emissions remain capped under the EU ETS.

But electricity still accounts for only about 20% of Europe’s final energy consumption. The remaining 80% comes from molecules such as oil and gas. In the long run, hydrogen may help decarbonise these fuels, but in the medium-term gas savings and biogas are better placed to reduce reliance on imported gas.

Since the 2022 energy crunch, European gas consumption has fallen from roughly 540 billion cubic metres (bcm) to 430 bcm, a reduction of 110 bcm, or 20%. Even so, Europe still imports about 70% of its gas, just over 300 bcm a year.

"Biogas is Europe’s scalable, local and circular medium-term gas solution. Hydrogen may help decarbonisation longer-term."

Today, biogas meets only 1.6% of gas demand. In theory, that share could rise to around a third if sustainable feedstocks such as manure, agricultural residues and organic waste were used more widely. Denmark shows what is possible: 58 plants built in a decade now supply around 40% of national gas demand, with potential to reach 100% in a few years if supported by additional policies. Still, security of supply and sustainability come with a trade-off as biogas is more expensive than imported LNG.

For more information, please contact Opens in a new tabGerben Hieminga, ING Research.

Gas demand is down 20%, but Europe still consumes 430 billion cubic meters a year.

ING & Climate

Society is transitioning to a low-carbon economy. So are our clients, and so is ING. We finance a lot of sustainable activities, but we still finance more that’s not. See how we’re progressing on Opens in a new tabour climate approach.

Authors

Peter Kindt

Global Head Sustainable Solutions Group a.i., Head Transition Accelerator

Arash Mojabi

UK Head Sustainable Solutions Group

Atrid Overeem

Editor, Global PR Manager Wholesale Banking

Henry Rushton

Sustainable Solutions Group - Energy Lead

Gerben Hieminga

Sector Economist Energy, ING Research

Timothy Rahill

ING Research