Cash Management in Focus: Trends Shaping the Treasury’s Strategic Outlook

6 October 2025

Reading time: 6 min

At times when digital innovation is rapidly accelerating and the regulatory frameworks across the EU and Switzerland are evolving, cash management is undergoing a profound transformation. This article offers a perspective on how treasurers can navigate disruption while aligning with both converging and diverging market dynamics, remaining at its position as a strategic enabler of resilience and growth.

Treasury teams play a vital role in maintaining a company’s financial health, turning business activity into actual cash flow and keeping payments secure. On top of internal challenges, treasurers must keep up with changing regulations, new technologies and global market shifts. The key is to separate meaningful opportunities from distractions, while managing day-to-day demands alongside long-term goals.

At ING, Transaction Services supports treasury teams driving progress with every heartbeat, through our global network, local expertise, tailored solutions, and lasting partnership. By providing stability through change, we help clients navigate complexities and prepare business for whatever comes next.

Focusing on the European Union (EU) and Switzerland, this article highlights the key developments shaping the environment corporate treasurers have to navigate, potentially impacting their European cash management. After providing the position and context of Switzerland for treasury operations, we will explore how external influences, such as regulatory changes, instant payments, digital currencies and financial autonomy, can influence treasury’s future strategic decisions.

Why Switzerland stands out

Switzerland offers a stable and well-regulated environment for treasury operations. Its strong economy, low inflation, and the Swiss franc’s reputation as a safe currency make it a reliable base for managing liquidity and risk and presents challenges that might be more strategic in nature. The country’s banking infrastructure is world-class, with Zurich and Geneva serving as major financial hubs. Real-time payment systems and deep capital markets continue to support efficient operations in Switzerland. Also, the Opens in a new tabSwiss Financial Market Supervisory Authority (FINMA) actively continues to pursue reforms to strengthen its supervisory framework and align more closely with global standards.

Strategically located, Switzerland provides seamless access to both European and global markets. Although not a EU member, it maintains strong financial interoperability through participation in systems such as the Single Euro Payments Area (SEPA) and TARGET2. Its political neutrality, combined with top-tier infrastructure and openness to innovation, makes it an attractive base for regional treasury centres.

The launch of the Opens in a new tabDigital Switzerland Strategy 2025 – which promotes AI, cyber-security, and blockchain in financial services – sets a clear direction for how the sector will adapt to emerging technologies. Treasurers are increasingly leveraging these tools to improve visibility, automate processes, and manage risk more effectively. In summary, Switzerland offers treasurers a compelling blend of stability, innovation, and strategic access. As regulatory and technological landscapes continue to evolve, Swiss-based companies are well-placed to lead in delivering efficient, sustainable, and forward-looking treasury operations.

Shared goals, diverging paths

The EU and Switzerland are both advancing digital in finance. Through its Digital Finance Strategy, the European Commission aims to reduce fragmentation, foster innovation, and prepare financial systems for technologies like AI and blockchain. Switzerland pursues its own digital agenda outside of the EU framework. While its goals – such as enhancing efficiency and advancing digitalisation – may align with those of the EU, the paths it takes to achieve them sometimes diverge.

Diverging paths can be shaped by different choices. The EU’s top-down regulatory approach to open banking contrasts with Switzerland’s market-led model, offering two distinctive perspectives. The EU’s PSD2 directive laid the groundwork for open banking, mandating access to account information and payment initiation for third-party payment service providers.

This has enabled new payment journeys and insights for companies. While choosing not to impose such requirements, Switzerland allows the industry to determine whether third-party payment service providers will obtain access to financial data.

Open finance can facilitate a new era of interconnectedness – enabling seamless data integration within financial services, and real-time insights that power innovative customer journeys and enhance B2B ecosystems. That includes moving from proprietary banking platforms to automated data exchange directly feeding in information to multi-bank software allowing for higher transparency, control and instant insight to further empower company’s data infrastructure. Both in Switzerland and in EU, corporate treasurers have started adopting APIs as connectivity method, but no structured change to treasury processes have been observed.

Although some trends are shared across borders, domestic standards still shape day-to-day operations. For example, Switzerland’s QR Bill simplifies invoicing and payments and reduces manual processing by embedding structured data in a QR code. This uniquely Swiss solution enables euro or Swiss franc payments through multiple channels. Its use of structured references supports automated reconciliation, enhancing efficiency and accuracy of domestic transactions. Making local payment methods available to clients of multinational corporations remains important to optimise incoming cash flows.

Changing the pace with instant payments

Open banking and APIs, combined with instant payments, help treasurers gain faster insights and better control over their funds. That is critical to unlocking the full potential of liquidity management. The SEPA Instant Credit Transfer scheme, introduced in 2017, was a pioneering step towards cross-border real-time payments in Europe. Now, Opens in a new tabInstant Payments Regulation (IPR) may be a catalyst needed to further drive adoption. Under IPR, Payment Service Providers (PSP) across the EU will need to support sending and receiving of euro-dominated instant payments, which are no longer capped at EUR 100,000. To mitigate operational risks and combat fraud, IPR introduces Verification of Payments (VoP). SEPA standard and instant credit transfers will be subject to additional checks confirming whether payee details match the account holder’s name and IBAN. Companies need to determine an approach for implementing VoP in the context of batch payments, as the regulation permits opting out of performing VoP for each execution.

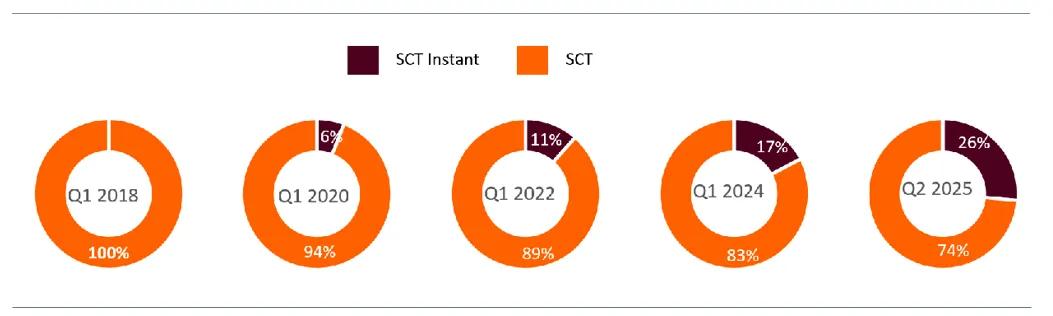

In Switzerland, instant payments are gaining ground, but adoption is slower. Since August 2024, the largest Swiss banks have been required to process instant payments, with all retail payment service providers expected to be reachable by the end of 2026. Until now, the absence of strong regulatory momentum may help explain why adoption in the Swiss market is limited. In May 2025 instant payments accounted for less than 0,5% of transactions, leaving the country behind the EU in leveraging real-time settlements where in 2025 the share of instant payments volumes amounted to over 26% of total SEPA credit transfers*. Factors such as the initially introduced transaction cap of CHF 20,000 (with potential for higher limits by agreement) and the lack of mandated fee parity may further deter broader use, especially for high-value and recurring B2B transactions.

Figure 1: Estimated share of SEPA Instant Payments volumes. Source: Opens in a new tabEuropean Payments Council

With both EU and Switzerland using regulations to further drive adoption of instant payments, when considering the ad- option of instant payments, the first step is validating whether there is a need for them in the corporate’s business processes. The benefits are compelling: no cut-off times to restrict transac- tion windows, the ability to collect cash from clients within se- conds, and the capacity to process time-sensitive transactions instantly, including instant customer refunds. They open oppor- tunities for enhanced liquidity management through real-time fund concentration across banks, entities, and borders. That is particularly valuable in times of heightened uncertainty and volatile market conditions.

Such benefits should be weighed against operational demands. The reduced processing time of instant payments limits fraud detection time. The treasury team might be forced to manage incoming transactions outside of standard working hours and decide whether this requires adjustments to internal processes. For positive confirmation with Verification of Payee, impeccable administration becomes critical. It all starts with putting correct names on invoices and updating own systems or banking applications. In that sense, VoP drives the need for data consistency and accuracy and supports reconciliation process efficiency.

While instant payments address the need for speed, most frameworks remain focused on domestic transactions – or, in the case of SEPA, regional ones. Cross-border payments, though evolving, continue to lag in terms of speed and efficiency. SEPA One-Leg-Out might become the way to receive instant cross border payments into the EU, depending on the ad- option by the banking community. Today’s technological advancements are challenging the traditional models of international settlement. Digital payments with stablecoins or CBDCs could be an alternative for both domestic and cross-border payments.

Towards a new digital ecosystem

Europe is actively exploring blockchain and its potential to sup- port the financial industry. Switzerland was among the first to regulate blockchain with its 2021 DLT Act and continue driving digital innovation in financial industry through experimenting with digital assets. The EU has followed with MiCAR, which is expected to accelerate the adoption of digital payment methods by providing regulatory clarity.

Digital assets benefit from blockchain characteristics that are promising for financial services. For example, with its ability to process transactions instantly, this technology should address one of main pain points of cross-border payments. Programmability allows for automated execution based on predefined rules and immutability means that information added to the blockchain remains unaltered. Nevertheless, application of these benefits will have to be proven through experimentation and real-life use-cases.

At ING, we continue with our selective approach and experimental efforts focusing on validating professional clients’ demand and operational readiness. To do this, we actively seek collaboration with our peers to develop industry standards, bolstering trust, efficiency and scalability of infrastructure.

The digital ecosystem now includes digital identity. The EU’s Electronic Identification and Trust Services (eIDAS) regulation introduces the European Digital Identity Wallet (EU-DIW), providing individuals and businesses with secure digital IDs. Switzerland is developing its own system, with a referendum planned for September 2025. If adopted, the challenge will be ensuring compatibility with EU systems. A trusted digital ID could streamline know your customer process, simplify document signing, and reduce risks associated with data transfer.

Time will tell how transformative regulatory developments truly are, reshaping the industry and introducing new tools. Shifts in market and geopolitical dynamics next to changing preferences may also act as drivers, prompting efforts to reduce fragmentation and enhance resilience at macro level. Digital payments can offer a key building block for new payment infrastructure, but building a robust infrastructure demands coordinated industry collaboration.

Strengthening integration and resilience

With new countries joining, the Single Euro Payments Area (SEPA) now includes 41 European countries further expanding reach of unified payment solutions. Only recently, the accessi- on of Bulgaria to the euro area was approved, effective 1 January 2026. For treasurers, this may prompt a reassessment of cash management structures, including centralising euro flows, redesigning account structures to rationalise bank accounts and banking partners, and adapting internal systems to new reporting and liquidity requirements. With the broad pan-European reach, SEPA improved efficiencies between Payment Service Providers (PSPs), especially in terms of settlement.

On the other hand, globally, the decline in cash usage has accelerated the shift toward digital payments, particularly for retail transactions. This has raised questions about monetary sovereignty and the role of central bank money as a financial anchor.

Figure 2: Types of instruments used in Point-of-Sale transactions in euro area (Source: ECB, ING)

On top of minds now is the EU pilot aimed at developing a retail central bank digital currency (CBDC) for retail and businesses. Initially, the project focused on safeguarding the role of central bank money in an increasingly digital economy. However, with rising geopolitical instability, the focus has shifted towards reducing Europe’s dependence on international card schemes, strengthening the euro’s position, and reinforcing the EU’s ‘open strategic autonomy’. At the same time the European Payment Initiative initially with support from French, German, Dutch and Belgian banks is looking to offer peer-to-peer, online and in-store payment solutions that can compete with card schemes. For corporates in the B2C space this may offer an additional means of collecting cash in Europe. Switzerland is following its own path with the Project Helvetia, focusing exclusively on a wholesale CBDC, designed for interbank transactions rather than retail use. With the project Switzerland aims at making financial market infrastructure more secure and efficient through blockchain-based solutions.

Strategic choices in building treasury strategy

From API connectivity, supplying insights to the business in a real-time, accelerating payment flow and funds concentration to testing new payment instruments the European financial industry unlocks opportunities for treasury that go beyond the daily practices. With developments across infrastructure, regulation, and technology the key is to make smart, strategic choices and pursue trends that are aligned with business goals.

Despite the continuous effort to integrate infrastructure across Europe, treasurers still need to manage market specific characteristics as international context comes into play.

Treasury is at the heart of every organization, offering insights, liquidity, and resilience to every strategic decision. We stand by our clients through committed and trusted partnership, jointly seeking ways to drive progress as we believe progress is always possible and best achieved together.

*Source: Opens in a new tabEuropean Payments Council, SEPA Instant Credit Transfer

Authors

Annelinda Koldewe

Global Head, Payments & Cash Management, ING

Natalia Heidendal

Head of Transaction Services, ING Switzerland