ING Sustainable Finance Pulse - issue 8

27 November 2025

Reading time: 8 min

Welcome to ING’s Sustainable Finance Pulse - quarterly glimpse into the world of sustainable finance and ING’s take on it.

In this issue:

The sustainable finance market maintains momentum for the first 3 quarters of 2025. Looking at 2025, we believe the issuance volume so far indicates a robust global sustainable finance market, especially in light of global policy and geopolitical uncertainty.

ING sees another strong quarter in sustainable finance activities.

This Sustainable Finance Pulse also highlights the topic of data centres & energy. With increasing use of AI, data centres' need for energy efficiency is evident. ING supports clients in this intersection through financing, deep sector knowledge and sustainability expertise.

1.0 Sustainable finance market maintains momentum in Q3 2025

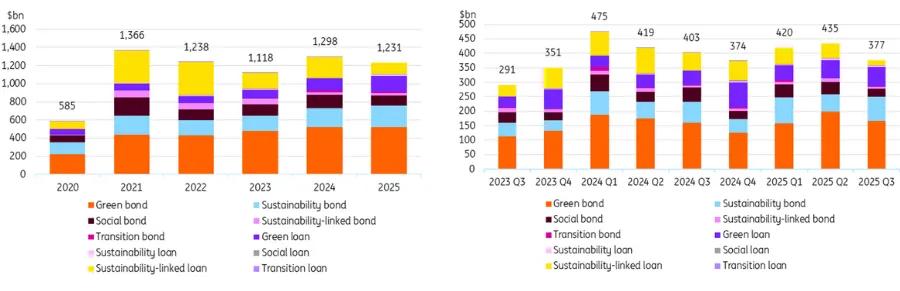

The global sustainable finance maintained solid momentum in the first three quarters of 2025, with issuance reaching $1,231bn. This figure is slightly below the $1,298bn in the same period of 2024, but higher than the level in 2023.

Yet, Q3 of 2025 itself was softer, with issuance totalled $377bn, down 14% quarter-on-quarter decrease. Issuance in Q3 of 2025 is also 6% lower than in Q3 of 2024, but substantially higher than the $291bn of issuance in Q3 of 2023, the lowest in all quarters since 2023.

Green bonds remain the most popular instrument, with issuance in Q1-Q3 this year surpassing the level in Q1-Q3 of 2024. Green loans show strong year-on-year growth, with several sizable deals from corporates globally.

Sustainability bonds are also trending strong, posting their second-highest Q3 issuance since 2023. On the other hand, social bonds, sustainability-linked bonds (SLBs) and sustainability-linked loans (SLLs) declined year-on-year, though we believe BNEF data does not capture all private deals. Our own analysis supports a positive outlook for sustainability-linked loans globally, despite US weakness. Transition debt slowed as well, mainly due to reduced sovereign issuance in Japan after its surge in 2024. Still, countries such as Australia, Thailand, and India have also established transition taxonomies, signaling future issuance increases.

Looking at 2025, we believe the issuance volume so far indicates a robust global sustainable finance market, especially in light of policy and geopolitical uncertainty in many parts of the world. We are hopeful that the full year issuance in 2025 can be comparable to that in 2024.

As in the previous issue of the Sustainable Finance Pulse, our figures exclude asset-backed securities (ABS), though we note encouraging progress in sustainable ABS globally.

It is important to note that sustainable finance market sentiments continue to diverge across regions. With $345bn of issuance in Q1-Q3, APAC is seeing consecutive annual growth since 2021 and on track for another record year. In EMEA, the $592bn of issuance in Q1-Q3 of 2025 falls short of the $634bn seen in 2024, but the region’s Q3 of 2025 outperformed Q3 of 2024. The US posted a stronger Q3 than Q2, but total issuance of $240 billion for Q1–Q3 still lagged last year’s level. Most activity came from US-based supranationals, while private issuers remained cautious.

Source: ING Research, BNEF

We do see positive drivers for sustainable finance heading into 2026:

- Corporates remain committed to decarbonisation, creating financing needs to realise interim climate targets.

- The emerging megatrend of AI and data centres will spur the demand for renewable energy.

- Renewed country-level climate ambition from COP30 can encourage more sovereign sustainable issuance.

- Continuously developing regulations in many countries will enhance market transparency and standardisation.

- Increasing extreme weather events can prompt public and private issuers to mitigate and manage climate risks.

Global Head Sustainable Solutions Group

Jacomijn Vels

"This year’s strong growth in sustainable finance highlights our clients’ determination to build a more sustainable future. The surge in green lending and focus on sustainability show that sustainable finance drives both business resilience and value. ING is committed to supporting our clients in achieving their climate ambitions"

ING Sustainable Finance transactions*

* Nr of sustainable finance transactions of 4 key products for ING

2.0 ING delivers robust growth in Q3 2025

ING delivered a very robust quarter, mobilising €110bn of sustainable finance 9M2025, a 29% increase compared to 9M2024 (€85.3 bn)**. This was driven by solid performance across three quarters, with Q3 2025 contributing €43.3bn (+54% vs Q3 2024).

Green loans have surpassed sustainability-linked loans as the leading product category by number of transactions, followed by sustainability-linked loans and green bonds. The uptick in green lending has been seen across all regions driven by renewables and strong demand for highly efficient data centres and real estate.

The number of sustainable finance transactions and volume mobilised increased across all regions:

- We see continued growth in APAC driven by strong client demand for sustainable finance products.

- Americas held up well, despite geopolitical uncertainties, with a lot of activity with clients in the data centre sector who have been in a stage of exponential growth but looking for ways to overcome challenges in access to energy.

- In EMEA we see healthy deal flow with continued client commitment to sustainability and the transition driving sustainability-linked and green lending volumes.

The EMEA region remained the largest contributor to volume mobilised at 62%, followed by the Americas (24%) and APAC (14%).

Despite global geopolitical uncertainty and debates over climate policy, recent surveys of C-suite executives show that sustainability remains a top strategic priority. As also outlined in the article Opens in a new tab"From Belém to the boardroom – what COP30 means for climate leadership" from ING Research. However, leaders must navigate these efforts alongside challenges like trade disputes and political instability.

The surveys referred to in the ING Research article, also show CEOs increasingly see sustainability investments as boosting financial performance, with revenue generation now the top benefit over compliance or cost savings. They are prioritising initiatives that directly enhance business value, such as resilient supply chains, circular economy practices, and sustainable product innovation.

Prioritising sustainability helps corporates access green financing, manage risks, and seize low-carbon market opportunities. ING is committed to enabling this transition with innovative products and advisory services, supporting clients in achieving their climate goals.

** For more information and a full list of products please see: Opens in a new tabPerformance and reporting | ING

3.0 Beyond storage: the sustainable transformation of data centres

Data centres and sustainability are linked by the increasing demand for digital infrastructure, which has significant energy and resource requirements. However, data centres are becoming more sustainable by adopting energy-efficient technologies like advanced cooling systems, switching to renewable energy sources, and repurposing waste heat for local communities.

Relevance for the economy

Data centres provide the computing power needed for the storage, transport, and processing of our data. That may sound abstract, but data centres are the engine of our digital world, as they offer the computing power that our digital lives require. In doing so, they not only allow us to endlessly watch cat videos, but they also keep hospitals online, enable internet banking, and provide the computing power required for new digital developments, including generative AI. Data centres are thus vital for businesses across all sectors of the economy.

Financing more sustainable data centres

The way data centres are funded is changing quickly because digital data is growing fast, especially with more digital services and the rise of artificial intelligence. By 2030, the amount of digital data is expected to be over 20 times higher than it was in 2018. This means more and bigger data centres are being built. As a result, there is more demand for land and electricity, and it costs more to build these centres because of higher prices and construction costs.

To deal with these problems, investors are looking for new ways to pay for data centres, depending on how developed each region’s market is and how much competition there is. In the United States, the market is more developed and uses advanced financing methods such as asset-backed securitisation (ABS), which is used more as data centres move from being built to being fully up and running. The US uses ABS more often because it has a lot of data infrastructure. Europe is starting to catch up, for example with ING helping lead the first euro-based ABS deal for data centres. This was a €640 million project with Vantage Data Centres in 2025.

Innovation and co-location

As data centres use more power - the International Energy Agency expects a 130% increase by 2030 from today’s level - there is more focus on their impact on the environment. This has led to a stronger push for renewable energy, such as solar power, which is getting cheaper, can be expanded easily, and does not create direct emissions. In some places, new data centres are being built right next to new solar power plants. For example, in the Middle East, many new data centres are being connected directly to solar panels. Besides using renewable energy, improving efficiency is also important. New technology such as photonic chips can save more energy and work better than traditional fibre optics. Also, large data centres can help stabilise electricity supplies because they use a steady amount of power, which is helpful as more renewable energy is used.

Financing sustainable data centres focuses on efficiency, emissions, water use, renewables, energy reuse, and waste reduction. Power Usage Effectiveness (PUE) is the key metric, which measures a data centre’s total energy use compared to the energy consumed by its IT equipment. While IT energy use depends on clients, operators can control major factors like cooling, and using more efficient systems can lower costs and boost competitiveness.

ING leading the charge

ING is a pioneer in data centre financing, with over 200 data centre deals completed worldwide. ING is not only one of the biggest financiers for both the energy and data centre sector, we have also been closely monitoring their intersection and established ourselves as a thought leader in this space. As data centres use more energy and have a bigger impact on the environment, ING is helping make sure the money it provides encourages operators to cut greenhouse gases and meet important environmental and social goals. ING’s latest deals show the data centre sector remains serious about sustainability, with green and sustainability-linked financing increasing across the globe.

Deal highlight

ING acted as Joint Sustainability Coordinator on AirTrunk’s $2.24bn facility to build its green data centre in Singapore. AirTrunk is a hyperscale data centre operator in the Asia-Pacific & Japan region, developing and operating data centres with industry leading reliability, technology innovation and energy and water efficiency.

4.0 ING Research: Digital growth, more sustainable power: data centres at the forefront

As the digital economy expands, the environmental impact of data centres has become a critical concern for both industry leaders and policymakers. Three recent articles by our research colleagues explore how data centres are leveraging innovative approaches to balance their soaring energy demands with the need for sustainability and community benefit. From purchasing renewable electricity to onsite power generation, increased demand flexibility and advanced heat reuse systems, these developments reveal the sector’s potential to drive broader energy transformation.

Onsite power generation

Meta, Amazon, Google and Microsoft are leading the way as the largest purchasers of renewable power purchase agreements (PPAs) in 2025, with the power mostly sourced from solar and nuclear power stations, with wind farms following closely behind. Traditionally, this renewable electricity has been supplied to data centres via the power grid; however, there is a growing trend of data centre developers investing directly in onsite power generation. This includes expanding their portfolios in renewable energy projects as well as in gas-fired power plants, some of which incorporate carbon capture and storage technology, demonstrating a commitment to both sustainability and energy security.

Alleviating the grid

Another significant development is the growing role of demand flexibility in enhancing power system efficiency. Data centres, as large and consistent energy consumers, can voluntarily shift non-urgent workloads to off-peak hours, alleviating stress on the grid. For instance, Google recently announced plans to move some machine learning operations away from periods of peak demand, while Aligned Data Centers is investing in substantial battery storage to increase their demand flexibility at a new facility in the Pacific Northwest.

Re-using heat

A key focus is the underused potential of capturing and repurposing surplus heat produced by data centres. Traditionally, vast amounts of heat produced by servers are simply expelled outside through cooling systems, wasting a valuable resource. Now, progressive data centres are adopting heat reuse systems that redirect this thermal energy to nearby homes and industries for water and space heating. While the siting of data centres near heat consumers poses challenges, this approach is gaining momentum in Europe. Notably, Google’s data centre in Skein, Norway is pioneering this model by aiming for 99% carbon-free electricity and using advanced systems to recycle heat within the local community.

Spider in the transition web

Despite these advances, challenges remain. Renewables are an unstable power source and not all data centre workloads are suitable for flexible scheduling. Furthermore, regulatory frameworks are still catching up with these technological shifts. However, as the sector continues to grow, so does its responsibility and opportunity to contribute to local and global sustainability goals.

Read more about data centres on Opens in a new tabING THINK.

ING & Climate

Society is transitioning to a low-carbon economy. So are our clients, and so is ING. We finance a lot of sustainable activities, but we still finance more that’s not. See how we’re progressing on Opens in a new tabour climate approach.

Authors

Hans van Uffelen

EMEA Head TMT & Healthcare

Gerben Hieminga

Sector Economist Energy, ING Research

Astrid Overeem

Editor, Global PR Manager Wholesale Banking

Ouafaa Najim

Global Sustainable Lead TMT, Sustainable Solutions Group

Arash Mojabi

UK Head Sustainable Solutions Group

Wim Steenbakkers

Global Lead Satellites & Technology

Coco Zhang

ESG Research, ING Research