The AI race is driving TMT debt issuance

7 July 2026

Reading time: 3 min

AI platform competition is accelerating, driving increased investment in technology, media, and telecommunications. Though much capex will still be funded by operating cash flows, the sector is set to dominate 2026 debt markets with roughly €55bn of additional issuance in Europe and at least $50bn in the US

We’re seeing aOpens in a new tab race to dominate the AI platform infrastructure, with operators of large technology platforms ramping up investments. We expect technology, media, and telecommunications (TMT) issuers to account for a large share of the €485bn total credit issuance expected for 2026. Given year-to-date issuance, we expect the TMT sector to raise an additional €55bn from European debt markets this year. Given upcoming redemptions, we expect at least an additional US$50bn to be raised by TMT issuers in US credit markets. In this note, we provide updated figures while maintaining our view that a large share of the investments by the large technology platforms will come from operating cash flows.

AI revolution translates into strong revenue growth

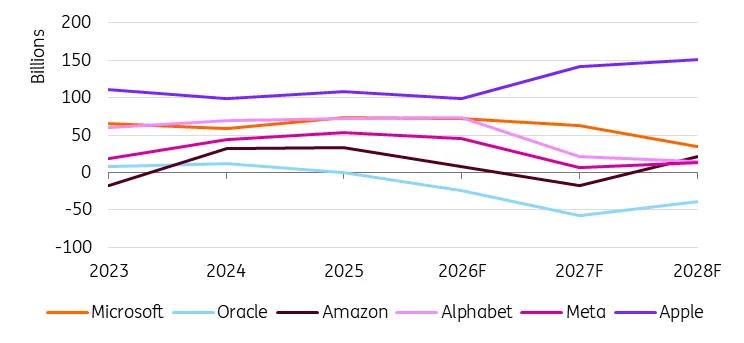

The Gen AI revolution was initially met with scepticism, with investors questioning whether heavy spending would generate meaningful returns. Today, however, the largest technology platforms are reporting strong AI-driven revenue growth.

Although this performance is still largely driven by strong growth in their Cloud businesses, TMT companies are already seeing growing revenue contributions from AI-based lines of business. Moreover, the market expects revenues from the largest technology platforms to rise even further. We agree with this view. Consensus revenue growth expectations are shown in the figure below. In our view, revenue growth is real, on both a historical and forward-looking basis.

Technology sector continues to show strong revenue growth (USD)

Organic cash generation remains impressive and can cover investment requirements

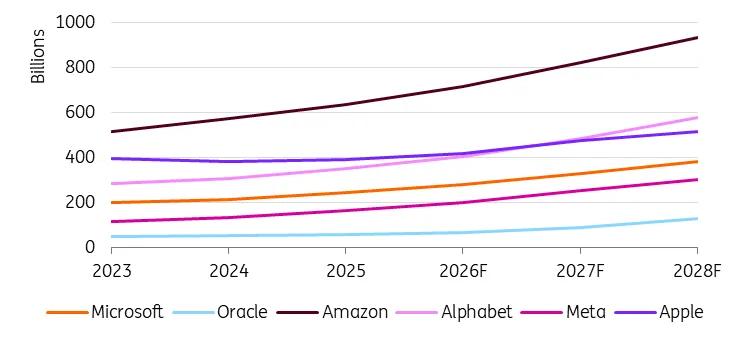

We continue to expect this strong revenue growth to support a further increase in operating cash flow. This is especially important as companies ramp up capital expenditure. As can be seen in the chart below, the world’s largest technology companies are expected to invest more than US$700bn in fiscal year 2026 – approximately a sevenfold increase since 2021.

Capital expenditures are rising quickly (USD)

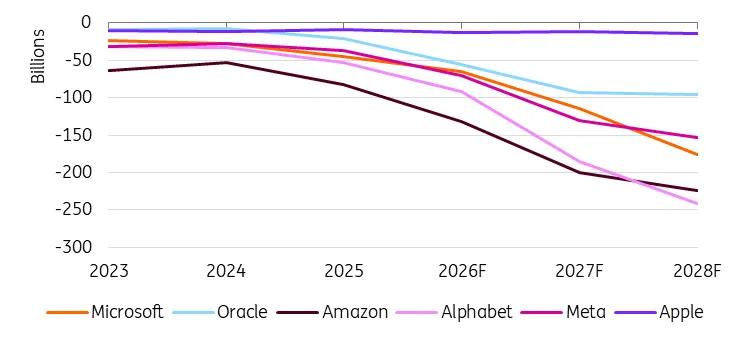

One of the positive elements of accelerating spending plans to fund the AI infrastructure build-out is that they can largely be funded by growth in operating cash flow.

Most technology platforms generate solid cash flow (OCF – Capex) (USD)

TMT companies continue to raise cash in debt markets

Since companies can fund most of their investments with operating cash flow, why would they turn to debt markets to raise capital? First, based on low leverage, companies such as Alphabet and Amazon have room to issue more debt within current rating metrics.

Second, because demand for AI services exceeds supply, and large technology platforms are looking to expand capacity. They can potentially accelerate the build-out through issuing debt, thereby capturing capacity-based market share.

Third, we think capital markets are open and see an opportunity for these companies to raise more debt. Companies need to do this strategically to avoid market saturation. When they raise debt diligently, they can avoid paying high new issuance premia. This is also why it matters to be first to market.

Fourth, we expect companies to be keen to resume share buybacks when they have the opportunity to fund them. This would be an additional reason to issue debt. At this point, it's difficult to forecast the total market share buyback amount. Part of the uncertainty stems from other cash flow items, such as potential acquisitions. It also arises from the expansion of investment plans. We see these investments as a strategic game in which no company wants to fall behind. As such, companies are looking to reduce operating costs, freeing up more money to allocate to investments.

The race to expand capacity is also constrained by physical supply limitations. Not all vendors can meet demand, while permitting processes take time. As investment plans are regularly revised higher, there is less cash left for share buybacks. As such, we expect companies to seek maximum financial flexibility, including debt issuance, to increase capital spending within current rating limits.

In the following two sections, we describe the room individual issuers have, as well as how additional issuance will look within the wider credit markets.

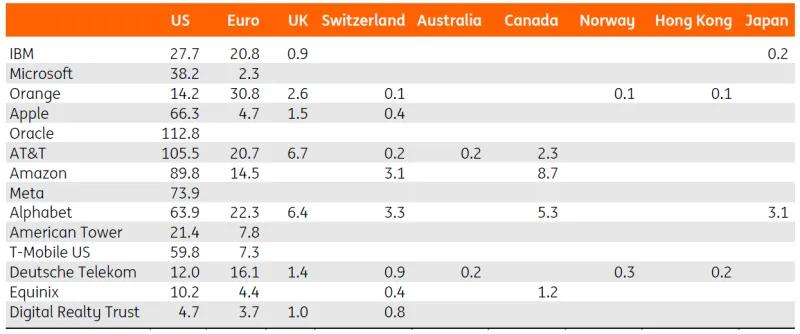

For TMT, total outstanding debt is largely denominated in US$ and euros (€bn)

Individual issuers also have room to raise more debt

Technology companies have historically raised most of their debt in US and European capital markets. Here, we argue that tech firms can raise at least as much as incumbent telecom operators. As shown in the chart above, Oracle and AT&T have issued roughly €110bn of notes in the dollar market, while Orange has raised €31bn from European markets. As most technology platforms, including Alphabet and Amazon, have industry-leading ratings, we see scope to raise similar amounts across Europe and North America and even more in the coming years. The share of AT&T in the “iBoxx $ Corporates” benchmark is only 1.02%; Oracle’s share is 1.22%. We argue that issuers have scope to raise even more debt even if asset managers start imposing single-name issuer benchmark caps. Because a 3% cap is standard in customised high-yield indices, there’s still ample room for tech issuers to add more debt. Orange’s share in the iBoxx € Corporates benchmark is currently 0.79%.

As can be seen in the chart above, TMT issuers are also tapping markets beyond the US and the EU – notably the UK, Switzerland, Canada and Japan. We expect this trend to continue as companies look to diversify funding sources. Although relative funding costs matter, we think the desire to tap multiple investor pools drives the decision to look elsewhere. The US and EU remain the most important markets for funding.

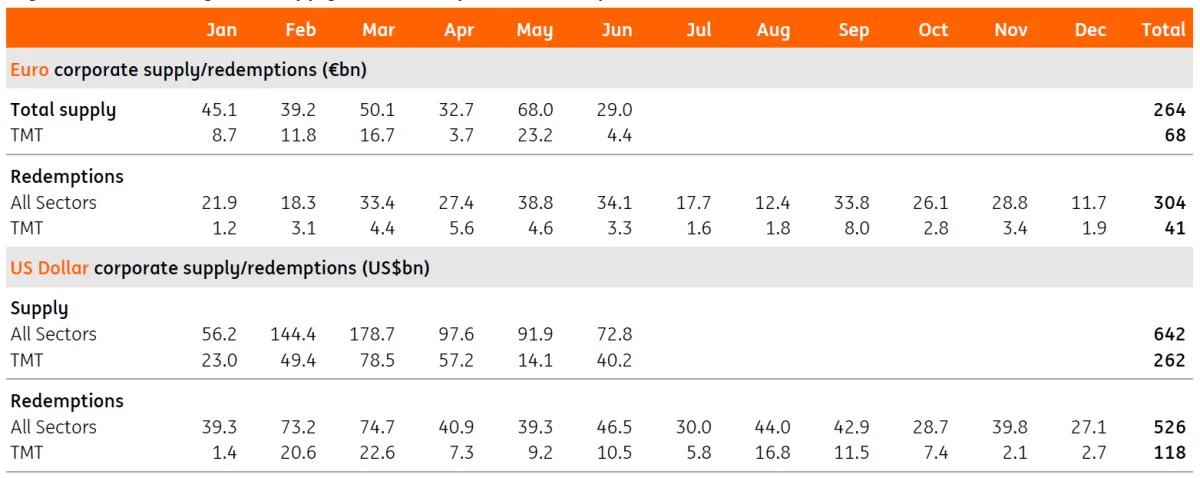

2026 monthly bond supply (incl. redemptions) in Europe and the US

How does this impact overall credit supply figures?

Looking at overall FY26 corporate supply, we remain supportive of robust issuance across European and US credit markets. This is driven by substantial deals from US tech issuers, also leading to robust Reverse Yankee supply. Another factor prompting high supply is the relatively large number of bonds coming due in FY26 (the elevated level of redemptions can be seen in the figure above). Issuance volumes are therefore expected to remain elevated for the remainder of FY26, reaching the overall supply forecast of €485bn for European markets. We expect roughly 25% of this supply to come from the TMT sector, or €121bn for FY26. Net total supply is set to remain broadly stable at around €180bn, in line with 2025 levels, influenced by elevated FY26 bond redemptions (about €304bn).

Corporate supply in Europe year-to-date is already at €264bn. This figure is materially higher than in previous years (except for 2020). Markets in the USA show similar trends; YTD supply amounts to US$642m, also ahead of previous years (except 2020). Interestingly, 41% of YTD supply in the US comes from the TMT sector. We expect robust TMT issuance in the US for the remainder of the year. Upcoming redemptions mean that US$ supply should be at least US$50bn.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.

Author

Jan Frederik Slijkerman

Senior Sector Strategist, TMT