ING Sustainable Finance Pulse - issue 9

18 March 2026

Reading time: 9 min

Welcome to ING’s Sustainable Finance Pulse - a quarterly glimpse into the world of sustainable finance and ING’s take on it.

In this issue:

- 1.0 Sustainable finance market set to grow

- 2.0 Strong Q4 for ING

- 3.0 Commercial real estate recovery in Europe

- 4.0 ING Research: Sustainability regulation at forefront for the real estate sector

The sustainable finance market remained resilient in the last quarter of 2025. Looking at 2026, we believe the issuance volume so far indicates a robust global sustainable finance market, especially in light of global policy and geopolitical uncertainty.

ING sees another strong quarter in sustainable finance activities.

This SF Pulse also highlights the topic of commercial real estate and how ING is supporting the transformation of the sector by financing energy-efficient upgrades and supporting the shift toward greener, low-carbon buildings.

1.0 Sustainable finance market set to grow in 2026

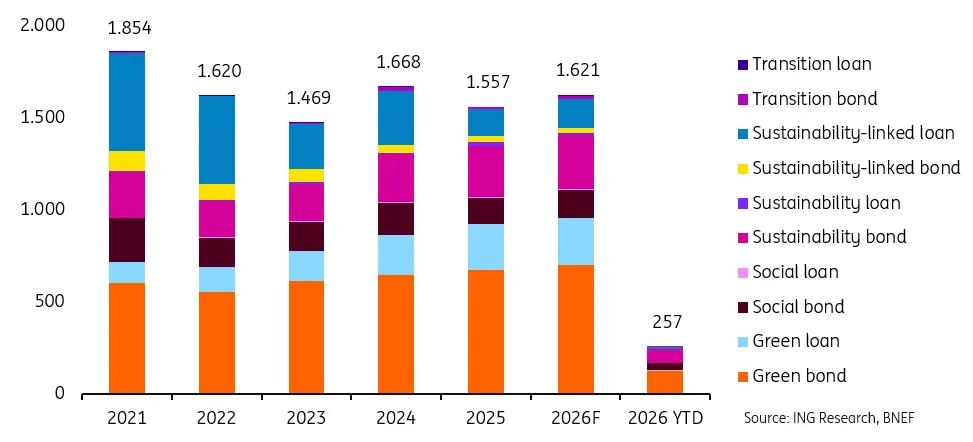

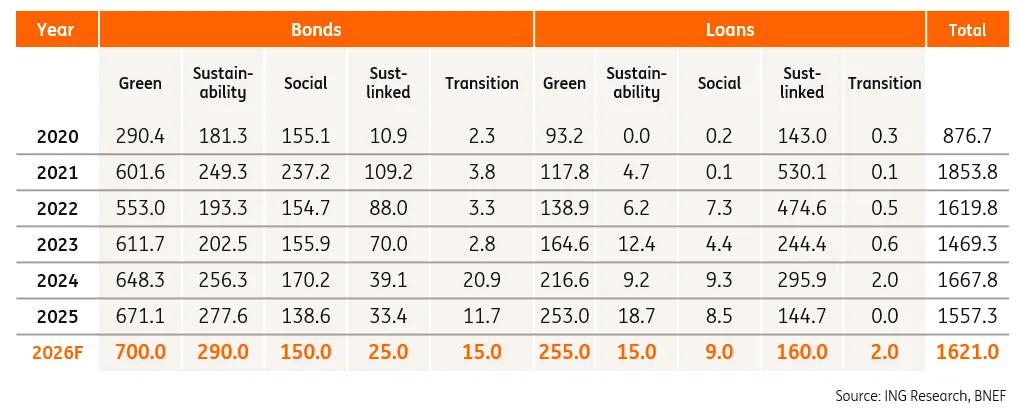

Global sustainable finance (excluding asset-backed securities, or ABS) is set to regain growth in 2026, surpassing the slight slowdown in 2025. Global markets ended last year with a total sustainable issuance of US$1,557bn , a modest drop from the US$1,669bn in 2024, but still comfortably above the dip in 2023. For 2026, we expect a rise once more, with issuance landing around US$1,621bn. This is still shy of the record 2021 figure, and long-term growth remains non-linear, but the market is showing resilience.

What is changing the most, however, is the underlying composition behind the sustainable issuance. The ingredients that make up this 'sustainable cocktail' are evolving, both in terms of regional outlooks and product choices.

When looking at issuance across regions, we are already seeing very mixed results.

- Europe, the Middle East and Africa (EMEA) is set to remain the largest region of sustainable issuance in 2026 with an expected rebound. By issuer type, governments and financial institutions are holding steady, while sovereigns, supranationals, and agencies (SSAs) show a small slowdown. But corporates have seen a notable dip. This is partially due to the ease of non-ESG debt issuance given strong investor demand, weakening the economic incentive for going Environmental, Social and Governance (ESG). Additionally, EMEA is already a well-established market for corporates with ESG frameworks, but the momentum may be softening. By product, sustainability-linked debt has been the weak spot. The sluggishness in corporate issuance and sustainability-linked products is a global trend. Even so, we remain optimistic about EMEA’s growth this year, supported by refinancing opportunities from maturing bonds and continued clean energy deployment.

On the other hand, sustainable issuance in Central and Eastern Europe is booming. It registered an impressive 40% year-on-year (YoY) growth in 2025, largely led by sovereigns and state-owned corporates. More robust growth in the sub-region is expected in 2026, contributing to EMEA’s overall positive outlook.

- The largest dip in global supply is evident in the US market, as policy swings have constrained issuance, given heightened challenges. The cut in tax incentives and funding, the rollback of regulations, and abandoned efforts to mandate climate reporting and federal DEI actions have created substantial uncertainty, leading issuers to adopt a more cautious stance. Within the US, corporates and financials have pulled back from sustainable issuance. While municipals have also seen a drop, supranationals have seen growth, boasting a notable 21% increase YoY. We expect US issuance to remain muted in 2026, though growing demand from the AI industry for efficient energy and expanded infrastructure can support sustainable issuance.

- Asia-Pacific (APAC) has continued to see decent growth over the past number of years with sustainable finance. 2025 ended in line with 2024’s figure. Green bonds and green loans saw strong growth YoY, while sustainability-linked loans and transition bonds experienced a small dip. Financials and corporates were the drivers of APAC issuance, while governments and SSAs marked a small decrease relative to 2024. In 2026, we expect to see more growth from APAC, and perhaps even a rebound of the transition bond debt.

While the ingredients to this sustainable finance issuance cocktail are changing in the form of regional differences and product choices, we still see ample reasons for future growth, and we have already seen a relatively strong start to the year with US$257bn coming to the market in the first two months. Of course, in March there has been a slowdown in issuance on the back of market volatility induced by the conflict in the Middle East.

- Many corporates stay committed to decarbonisation and managing climate risk.

- 2030 targets are still on the cards.

- Governments are using sustainable finance as a tool to fund decarbonisation efforts (despite the slight slowdown this year).

- Transition debt activities can rise as policy develops.

- The global journey towards sustainability is not linear but continues to advance.

- Regulation and standardisation provide clarity and ease.

Global sustainable finance issuance by product (excluding ABS)

Global sustainable finance issuance in numbers (excluding ABS)

Global Head of Sustainable Solutions Group

Jacomijn Vels

"The transition path is full of unknowns and can be messy, but it is also full of opportunity. We are helping clients cut through the disorder to manage risk, unlock value and protect it for the long term."

ING Sustainable Finance transactions*

* Nr of sustainable finance transactions of 4 key products for ING

2.0 ING delivers growth in Q4 2025

ING delivered a very robust quarter, mobilising €56bn in 4Q2025 (+ 29 % vs Q3 2025). With a total volume mobilised of €166bn in 2025, a solid 28% increase compared to 2024.**

Green loans continued to surpass sustainability-linked loans as the leading product category by number of transactions, followed by sustainability-linked loans and green bonds. The number of green loans increased 17% in Q4 vs the same period in 2024, contributing to a record number of green loans in 2025 for ING (up 45% versus 2024).

- In APAC, ING closed 2025 with record sustainable finance volumes, driven by strong performance in the first three quarters and leading roles in structuring deals as Sustainable Finance Coordinator. The market remained robust despite geopolitical challenges, with green bonds accounting for about 40% of activity and continued high demand for sustainability-linked loans. ING’s expertise was recently recognised with an industry award for ‘Green and Sustainability advisor of the Year’ by the Asia Pacific Loan Market Association.

- EMEA remained the largest contributor to ING’s sustainable finance volumes. The region experienced healthy deal flow and continued client commitment to sustainability and the transition, which fueled growth in sustainability-linked and green lending.

- In the US, private sector engagement in sustainable finance declined sharply due to political factors but increased social bond issuance by public entities kept overall volumes steady. ING’s expertise in renewables and data centers contributed to record deal volumes, helping clients find innovative energy flexibility solutions and maintaining its role as a preferred sustainability advisor.

The EMEA region led with 56% of mobilised volume, followed by the Americas (28%) and APAC (11%).

Despite geopolitical uncertainty and evolving climate policies, many organisations continue to prioritise sustainability as a key strategy. Clients are advancing sustainable initiatives amid challenges like trade disruptions and political instability, recognising that sustainability investments support long-term climate goals, competitive advantage, resilient supply chains, and innovation.

This focus enables companies to access green financing, manage emerging risks, and seize opportunities in low-carbon markets.

ING remains dedicated to supporting clients with financial solutions and expert guidance to help them meet their climate and business objectives.

** For more information and a full list of products please see: Opens in a new tabPerformance and reporting | ING

3.0 Sustainable finance fuels commercial real estate recovery in Europe

After the significant correction in 2023, Europe’s commercial real estate (CRE) sector rebounded steadily throughout 2025. Investor confidence returned as valuations stabilised and liquidity improved, leading to intensified competition for prime assets. The strongest demand focused on properties with high energy efficiency and clear sustainability credentials, while secondary assets lagged and required additional investment to meet new standards.

Shifting priorities

Sustainability has evolved from a compliance obligation to a key performance driver, reshaping the market’s priorities. Regulatory requirements such as the Corporate Sustainability Reporting Directive (CSRD) and the Energy Performance of Buildings Directive (EPBD), along with investor expectations, are reinforcing this shift.

Strong demand

ING’s 2025 activity reflects sustainability’s key role in our strategy, with 50 green transactions completed by year-end. Notable examples include the transformation financing of 40 Holborn Viaduct in London, which underscores the industry trend of high-quality refurbishments of well-located offices being among the lowest-risk deals, supported by strong pre-leasing and tenant demand. ING’s €815 million refinancing of ARES Fund V’s residential portfolio in Spain and Portugal, its €500 million green bond for NEPI Rockcastle in the Netherlands, and purpose-built student accommodation financing in Italy demonstrate how sustainable portfolios are attracting institutional capital.

Energy performance is key

These transactions highlight a market realigning around energy performance and climate resilience. Investors are seeking assets that can withstand structural shifts, and lenders are rewarding robust sustainability strategies.

Our CRE strategy focuses on helping clients transition to low-carbon buildings by prioritising assets with strong energy performance, enabling upgrades that improve efficiency, and integrating sustainability into financing solutions.

Performance is measured by the kilograms of greenhouse gas emissions associated with each square metre of a building or asset. We strive for a reduction of 56 percent by 2030, of which 8 percent has been achieved to date, and aim to reduce a further 48 percent.*

Transition trend

Looking ahead, ING will continue to partner with clients to help them in upgrading their brown assets, leveraging deep sector expertise to help transition portfolios toward greener, more resilient real estate.

As Sylvia Brandsma, ING’s Global Head of Real Estate and Infrastructure, says:

Our greatest impact is partnering with clients to assist them in upgrading their brown assets, using transition finance and deep sector expertise to help make their projects more sustainable.

*See more info in our Opens in a new tabAnnual Report 2025.

Deal highlight

ING, acting as Bookrunner and Mandated Lead Arranger, has underwritten a £170 million green loan to support the transformation of 40 Holborn Viaduct into one of London’s most sustainable office buildings.

The redevelopment will convert the property from a traditional brown building into a cutting-edge green workspace. Once complete, it will set a benchmark for energy-efficient, future-proof office space in the capital, incorporating advanced technologies and design principles that aim to reduce carbon emissions, optimise energy use and enhance occupant well-being.

4.0 ING Research: Sustainability regulation at the forefront for real estate in 2026

The European Commission estimates that buildings account for around 36% of greenhouse gas emissions (2021 data), making the buildings and real estate sector the single biggest emitting sector. The sector is thus a large piece of the puzzle for the EU in its push to reach net zero by 2050.

In 2026, multiple regulatory changes or updates are set to impact the real estate sector. From the Omnibus Directive on simplifying the CSRD & CS3D to the upcoming SFDR 2.0 revision to the Energy Performance of Buildings Directive (EPBD) transpositions, regulation around sustainability remains a key topic in 2026.

Physical climate risk concerns grow

According to PwC, concerns over physical climate risk are growing, with 83% of survey respondents noting climate risk is the second most important ESG credential for financing, behind energy efficiency. In Europe, physical climate risk is growing as climate impacts are being increasingly felt across the continent.

From wildfires to floods, risks are growing and becoming more frequent and are becoming increasingly relevant in property markets.

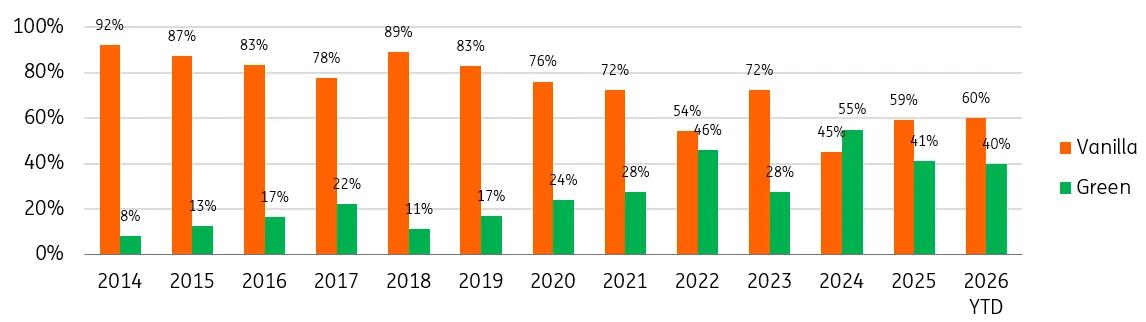

Real estate green bonds

Green bonds are an important tool for the real estate sector in its decarbonisation journey. In recent years, the level of green bond issuance has trended around 40% of total issuance by the sector, including so far in 2026. While this is below the 55% record level we saw in 2024, the data indicates that green bond issuance has grown to become a significant part of total real estate bond issuance and is set to remain there.

As shown below, the share of green bond issuance has increased from less than 20% in 2019 to around 40% currently. Ongoing refinancing needs and growth in sustainability investments and eligible assets supports this trend.

Source: Dealogic and Bloomberg

For more information, please contact Opens in a new tabJesse Norcross, ING Research.

ING & Climate

Society is transitioning to a low-carbon economy. So are our clients, and so is ING. We finance a lot of sustainable activities, but we still finance more that’s not. See how we’re progressing on Opens in a new tabour climate approach.

Authors

Jacomijn Vels

Global Head Sustainable Solutions Group

Arash Mojabi

UK Head Sustainable Solutions Group

Astrid Overeem

Editor, Global PR Manager Wholesale Banking

Sylvia Brandsma

Global Head Real Estate & Infra

Alexander Piur

Global ESG Lead Real Estate Sustainable Solutions Group

Jesse Norcross

Sector economist Real Estate, ING Research

Timothy Rahill

ING Research