ING Sustainable Finance Pulse - issue 1

27 March 2025

Reading time: 6 min

Welcome to the first issue of ING’s Sustainable Finance Pulse, a quarterly glimpse into the world of sustainable finance and ING’s take on it.

Sustainable finance market

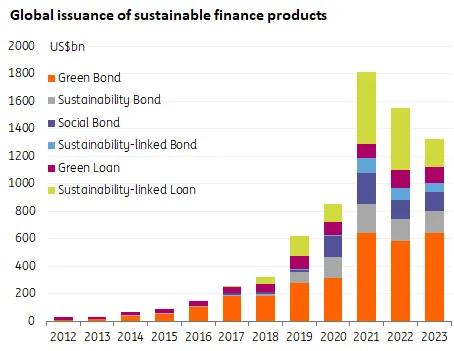

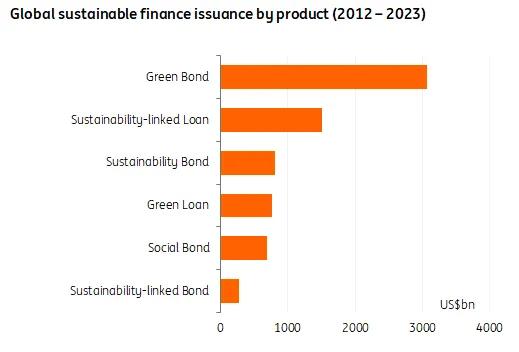

The sustainable finance market was confronted with a decrease in 2023 from 2022. According to Bloomberg New Energy Finance (BNEF), global sustainable finance issuance volumes amounted to US$1.3tr, down from US$1.55tr in 2022 and down on the peak seen in 2021 of US$1.8tr. With the exception of green bonds, most ESG debt instruments saw a decrease year on year. The largest decrease was observed in sustainably-linked (S-L) instruments, with S-L bond issuance falling 24% and S-L loan issuance falling by 55%. Only green bonds saw an 11% increase year on year.

Within global issuance for financial institutions, we see a small shift towards social bonds. This is driven by EUR issuance, where we also see an increase in sustainable bonds. Despite the slight decrease year on year, the preferred instrument remains the green bond.

Green bonds remain the preferred instrument globally for corporates, showing an increase in EUR green bond supply year on year. In 2023 we saw a small faltering of demand for sustainable finance debt, relative to the substantial demand seen in 2020-2022. This was mainly due to the slight investor pullback in order to re-assess the market, questions around greenwashing arose, increased pressure from lenders on materiality of target setting in sustainability linked instruments and more clarity on regulation was sought.

Source: ING Research, BNEF

This was evident in a slower level of inflows into the sustainable finance market and a lowering of substantial demand in the primary markets. In saying that, overall demand for sustainable finance products is still very strong. Looking ahead, we expect investors and lenders to continue to demand higher-quality structures, with increasing sustainability data disclosure requirements serving as an important tool to benchmark against.

Global issuance volume in 2024 is expected to continue to be lower than previous years and likely to be similar to volume seen in 2023. We believe similar trends will emerge throughout 2024 to those seen last year – leading to a relatively stable market compared to 2023. We forecast a global ESG bond supply of around €1tr for 2024, this is a relatively stable amount compared to 2023.

According to our ING estimates where we take a slightly smaller universe (of min €150m size and only self-labelled bonds), we should see sovereigns, supranationals, agencies, financial institutions and corporates issuing ca €325 billion in EUR. For the US dollar, we expect the market to stay stable at €225 billion (US$240 billion). For ESG bonds printed in other currencies, we expect the segment to grow softly from €260 billion to €270 billion. We outline more specifics of our forecasts in our report - Opens in a new tabGlobal ESG Bond Supply Outlook: Slowing down in 2024.

Source: ING Research, BNEF

Deal highlight - Decarbonising the steel sector

ING is very proud to have a leading structuring role in the project financing of the world’s first large-scale green steel plant of H2 Green Steel in Sweden. As per our work in developing the framework for Opens in a new tabThe Sustainable STEEL Principles, this is another example of how we’re helping to decarbonise the steel sector, and a great example that big steps can be taken in a hard-to-abate sector.

Going green isn’t always black and white. We will continue to support clients who are willing to transition, but increased scrutiny will likely also prompt tougher conversations on materiality and ambition of transition plans

Jacomijn Vels, ING’s global head of sustainable finance

The EUR 4.5bn multi-tranche financing includes more than 20 financial institutions, with ING acting as Documentation Bank and Senior Mandated Lead Arranger.

Want to know more about INGs view on the Sustainable Steel Principles? Contact Erik.van.Doezum@ing.com

ING grows sustainable finance in muted markets

High inflation and rising interest rates dampened loan demand considerably across all markets in 2023. In Western Europe, volumes in the general corporate loan market significantly reduced year-on-year, a trend that carried through into sustainable finance markets.

Yet the volume of financing ING mobilized, supporting our clients’ transitions to more sustainable business model, continued to grow to €115 billion in 2023 vs €101 billion in 2022, outperforming its 2023 target of €107 billion. The total number of sustainable finance transactions also increased, from 491 in 2022 to 792 in 2023, with ca 35% of transactions done via the sustainability-linked structure. Significant growth was achieved in green loans, growing in numbers from 63 in 2022 to 132 transactions in 2023.

Most of ING’s sustainable finance activity was in EMEA (66%), with sustainable finance transactions in APAC also gaining momentum. The Americas team managed to keep volumes relatively stable in the US, a market characterized by slowing environmental, social and governance (ESG) sentiment ahead of the 2024 elections and general uncertainty about the direction of the next administration.

Jacomijn Vels, Global Head Sustainable Finance: “What 2024 will bring is not easy to predict, remember that the outlook at the start of 2023 was for the Sustainable Finance markets to return to growth, instead we observed a second year of decline in volumes. Longer term the fundamentals however remain strong for a growth case for sustainable finance; increased regulatory support and reporting requirements combined with sustained commitment from investors towards sustainable investments.”

The main purpose of sustainability-linked transactions is to stimulate ING’s clients to step up their transition by linking their financing to their sustainability performance. According to Robert Spruijt, EMEA head of Sustainable Finance at ING, the 2023 drop in sustainability-linked volumes can be explained on the one side by the total syndicated loan market plunging in 2023, but also by the stricter guidance in the market for lenders around targets setting having had an effect. The latter we see as a positive development - as stated in our Opens in a new tabposition paper on the credibility of this market of 2021 - since stricter requirements on ambition & materiality levels will enhance the impact of the sustainability linked market.

ING Research highlight: plastics

Plastics producers in Europe face very ambitious carbon emission reduction targets. Scope 1 emissions fall under the European Emission Trading Scheme where, according to the current setup, CO2 allowances are phased out by 2040.

Luckily, there are technologies available to lower emissions by up to 75%, but they come at a serious cost, according to our recent calculations. The capture and storage of CO2 increases the cost of plastic production by up to 10%. Plastic recycling and switching from natural gas to electricity or green hydrogen to generate high-temperature heat could even increase production costs by up to 50%.

The irony is that a 50% higher price for a plastic bottle would barely increase the price you pay for your favourite soft drink. But such a cost increase is a big deal for European plastic producers, who play a small part in the entire supply chain and cannot charge consumer prices. In fact, they operate in international and highly competitive markets with little room to fully pass on higher production costs. It is hard to see very fast progress towards greener plastics on the supply side.

On the demand side, too, there’s room for less optimism as Europe’s new packaging waste law is not overly ambitious. The law intends to cut the amount of plastic by 10% by 2030, 15% by 2035 and 20% by 2040. Europeans would still consume 120 kilograms of plastic per year by 2040 if the target were to be met, which is twice as much as the current global average. So, despite some progress, the greening of the plastics industry is a process of evolution rather than revolution.

Society is transitioning to a low-carbon economy. So are our clients, and so is ING. We finance a lot of sustainable activities, but we still finance more that’s not. See how we’re progressing on Opens in a new tabing.com/climate.